Shortly before Christmas Micro Focus released their financial results for the six months to 31st October. Even with all the undoubted distraction that mergers and acquisitions cause Micro Focus still managed to increase revenues to $684.7m, 14.2% higher than the same period last year. The figures do include the trading results for Serena from when that acquisition completed in early May.

Key highlights for the period were strong performance by SUSE where revenues grew by over 23% while the Micro Focus portfolio of software solutions was ‘on plan’. The period saw improved cash generation in the company and other healthy financial indicators. Operating profit reached $163.3M against $150.4M in 2015. For shareholders the first half dividend has been increased to 29.73 cents per share from 16.94.

Company revenue is divided into license, maintenance, subscription and consultancy revenue which all saw good levels of growth. In the Executive Chairman’s report, Kevin Loosemore writes that Micro Focus is confident that the level of debt that the HPE merger will cause will not reduce the companies ability to deliver growth and that Micro Focus has ‘a strong operational and financial model that can continue to scale and produce excellent returns’.

Other interesting figures from the accounts indicate that geographically North America is the largest revenue centre at $359.7M followed by EMEA and LATAM at $257.7M and Asia Pacific & Japan with $67.3M.

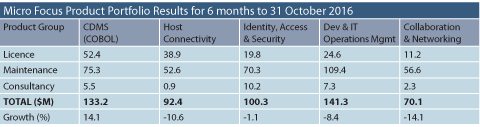

Delving deeper into the published figures we can look at the breakdown of the different product groups in the MF portfolio as the table below shows.

It’s disappointing to see the continued contraction of the Collaboration and Networking and IT Operations Management (including ZENworks) portfolios but it is in line with management expectations. We must hope for a turn around from this point onwards with the growth of Filr, ZENworks 2017 etc. In comparison the COBOL business is robust and Viusal COBOL revenues continued to grow strongly.

This article was first published in OH Magazine Issue 36, 2017/1, p24